Term Life Insurance

“Buy low with term to keep the family firm.”

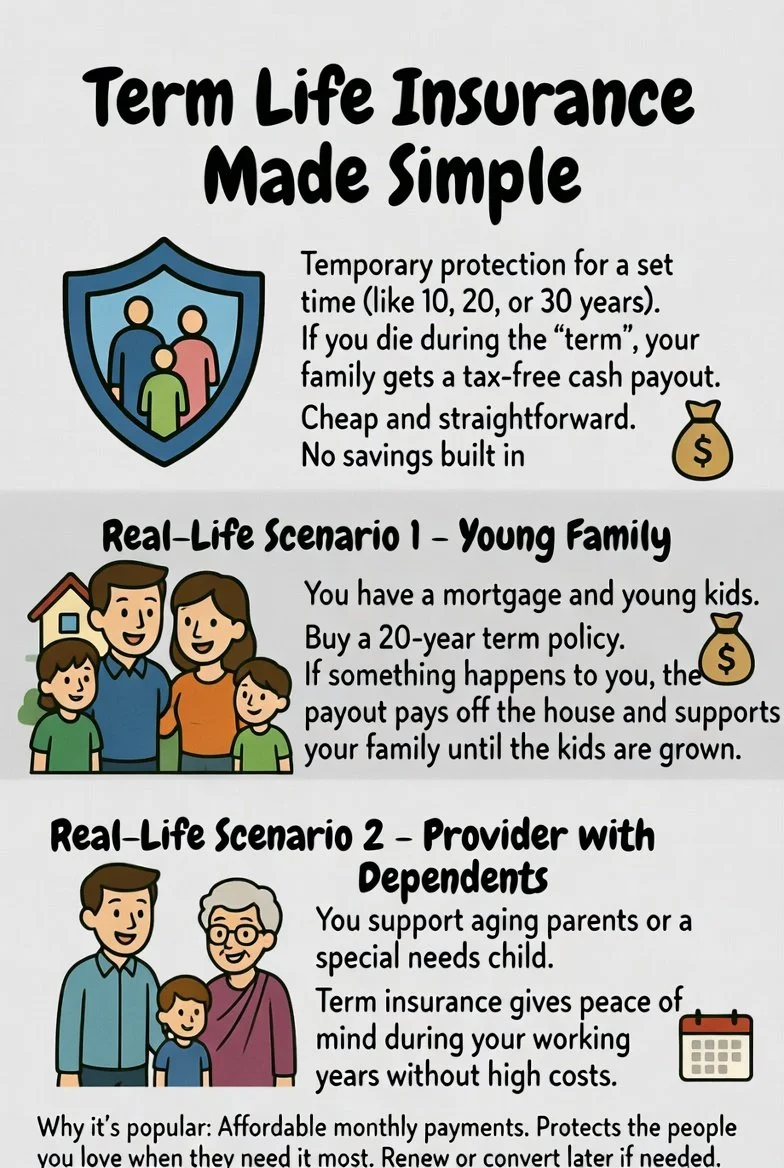

Affordable Protection for Your Family

Term life insurance provides guaranteed death benefit protection for a set period (10–30 years) with level premiums that do not increase. It is designed for individuals who want simple, cost-effective coverage to protect income, pay off a mortgage, or support dependents.

Ideal for families, homeowners, and working professionals, this policy offers high coverage at lower cost than permanent insurance, making it the foundation of most financial protection plans.

Real-world use cases: income replacement, debt payoff, college funding, and family financial security.

Policy Details & Specifications

Policy Type: Level Term Life Insurance

Term Length: 10, 15, 20, 30 years

Coverage Range: $50,000 – $50M+

Eligibility: Ages 18–75 (health & lifestyle based)

Riders: Accelerated death benefit, child rider, waiver of premium

Underwriting Type: Fully underwritten or accelerated (no-exam options available)

Why Choose Term Life Insurance

Term life offers the most coverage per dollar, with flexible terms aligned to financial obligations like mortgages or child-rearing years.

Better than alternatives: lower premiums, simpler structure, no investment risk.

Problems it solves: income loss, debt burden, financial instability.

Not ideal for: those seeking lifelong coverage or cash value accumulation.

Buying Guide & Comparison Insight

Top insurers such as Banner Life Insurance Company, Prudential Financial, and Mutual of Omaha compete on pricing, underwriting flexibility, and conversion options—making comparison essential.

FAQs

1. Is term life insurance worth it?

Yes—it's the most affordable way to secure high coverage.

2. Does it build cash value?

No—coverage only, which keeps costs low.

3. What happens after the term ends?

Coverage expires or can be renewed at higher rates.

4. Do I need a medical exam?

Often yes, but many qualify for no-exam underwriting.

5. How much coverage do I need?

Enough to replace income and cover major debts