Child’s Life & College Plans

“Save for school, play it wise, watch those funds begin to rise.”

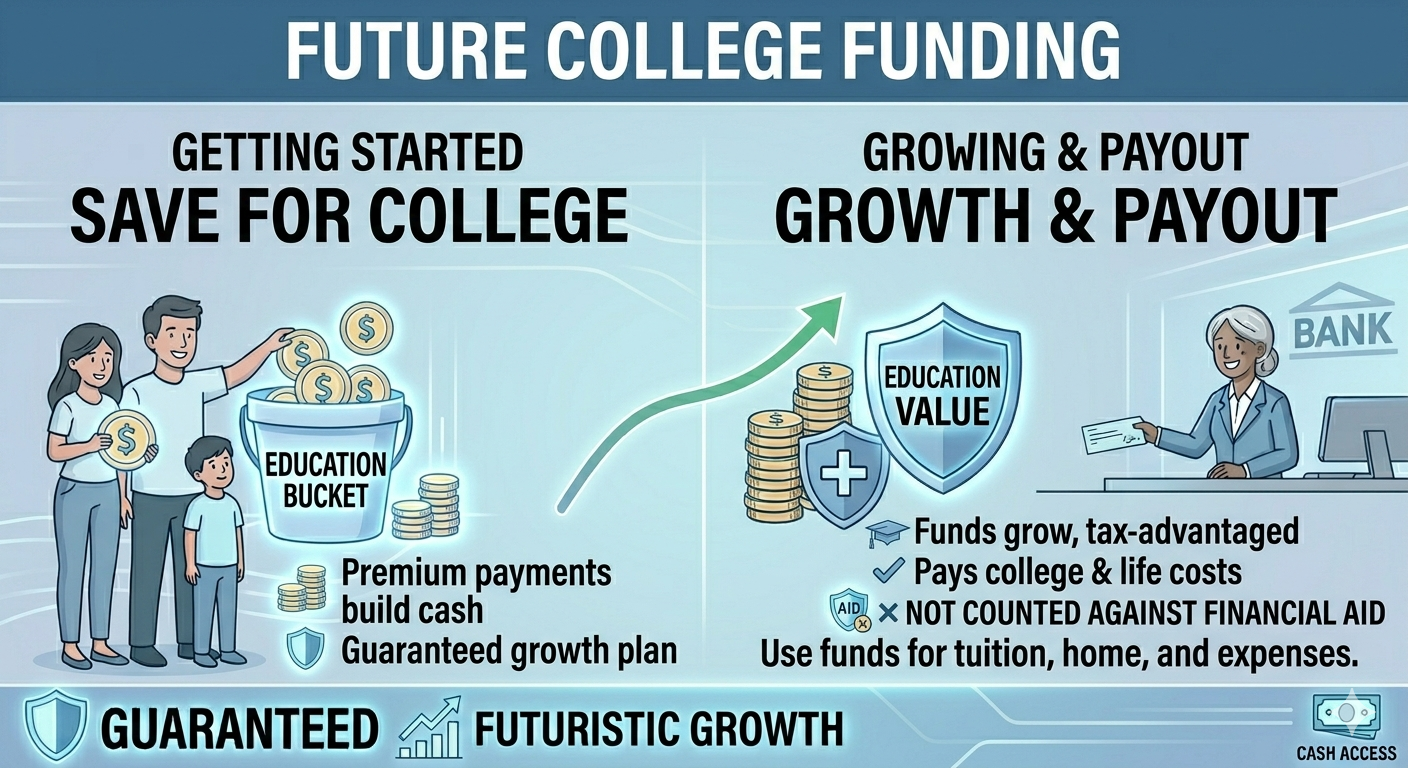

Protection + Future Financial Support

Children’s life insurance is a life insurance policy specifically designed for kids, typically whole life coverage that guarantees lifelong protection and may build cash value over time that can help with future expenses like college. It protects families while providing a financial foundation for children’s future needs.

This product is for parents, grandparents, and guardians who want to lock in insurability early, guarantee coverage regardless of future health issues, and potentially leverage cash value growth for education funding or other goals. Key benefits include affordable premiums, lifetime protection, guaranteed insurability, and increasing coverage options as the child grows.

Real‑world use cases: ensuring a child can always get life insurance later in life, creating a modest savings cushion for college or emergencies, and building tax‑deferred cash value.

Details & Specifications

Policy Type: Children’s whole life insurance or child rider attached to parent’s policy

Term Length: Lifetime coverage (permanent)

Coverage Range: Typically $5,000–$50,000+ depending on insurer and plan

Eligibility: Children from as young as 14 days to age ~17

Riders: Conversion options, increased coverage at specific ages

Underwriting Type: Simplified or no‑exam underwriting for kids

Why Choose This Product

Unlike adult life insurance, child policies guarantee insurability and often allow increasing coverage without exams later. They solve concerns about future health barriers and can serve as a disciplined savings vehicle with cash value growth.

Better than alternatives: more stable and guaranteed coverage than trying to buy insurance later in adulthood.

Not ideal for: families needing large college‑only savings—529 plans and dedicated college savings accounts typically outperform life insurance as purely educational savings vehicles.

Supporting Content & Buying Guides

Top rated children’s products include Mutual of Omaha, Gerber Life, and American Family, with features like flexible premiums, conversion rights, and coverage boost options as children age.

FAQs

1. Why buy life insurance for a child?

To guarantee insurability and build early cash value.

2. Does it help pay for college?

Cash value can be accessed for education expenses, but it’s not a dedicated college plan.

3. Is a medical exam required?

Generally no—child policies are simplified.

4. Can coverage increase later?

Many policies allow conversion or increased coverage.

5. Who owns the policy?

Parents or guardians usually own and manage it.