Group Life Insurance

“Protect your crew, keep business true, group life ensures success for you.”

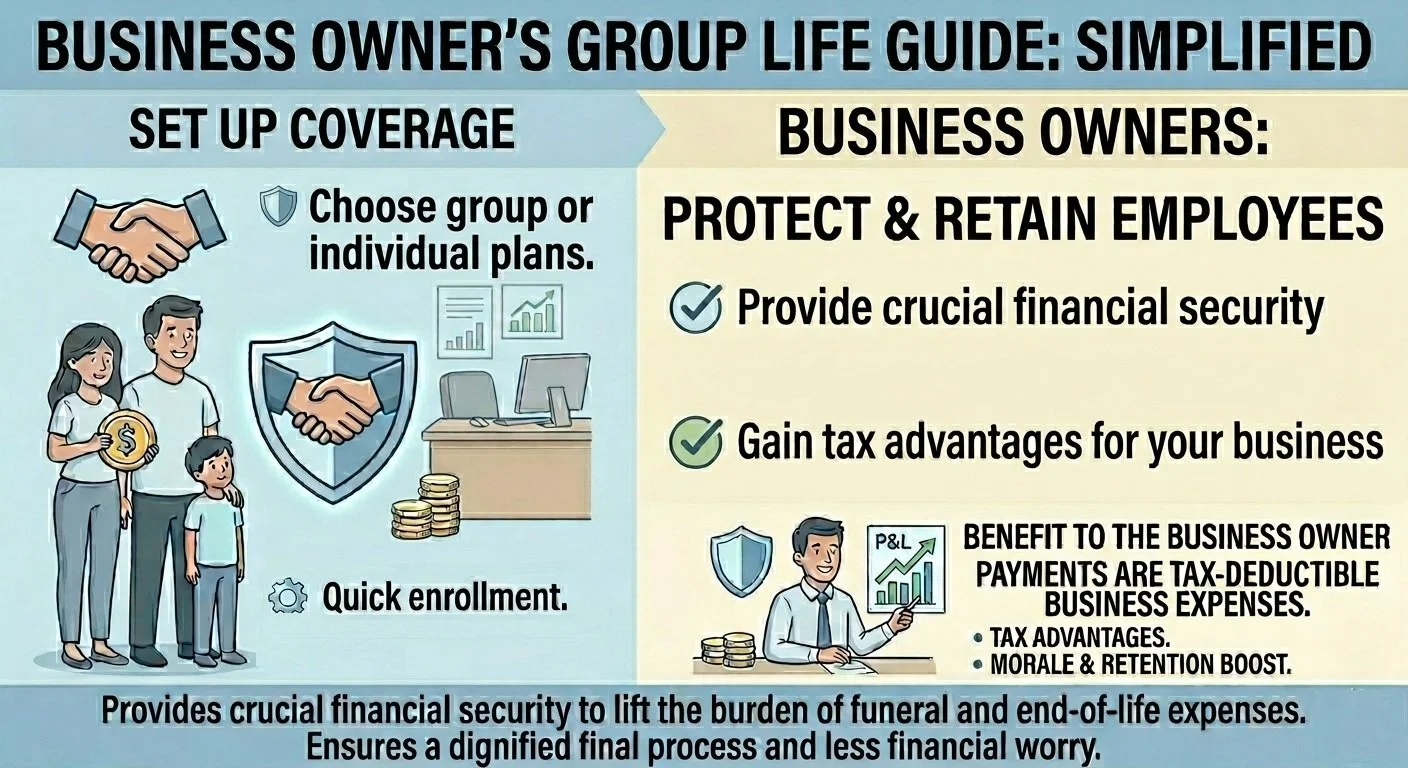

Employer‑Sponsored Financial Protection

Group life insurance is a life insurance benefit offered by an employer or organization to a group of employees or members under a single policy. It provides a death benefit to a beneficiary if a covered member passes away during the coverage period, giving families a source of financial support.

This product is for employers and employees, especially those building a competitive benefits package to attract and retain talent. Key benefits include lower premiums through pooled risk, simplified enrollment with limited or no medical exams, and broad coverage for workers at a lower cost than individual plans.

Real‑world use cases: supporting families after an unexpected loss, covering funeral expenses, and helping employees feel valued as part of a benefits program.

Details & Specifications

Policy Type: Employer‑sponsored group life insurance (often group term life)

Term Length: Typically tied to employment or membership duration

Coverage Range: Flat benefit amounts or multiples of annual salary (e.g., 1×–5× wages)

Eligibility: Active employees or members who meet employer/plan criteria

Riders: Optional add‑ons like accidental death benefit, spouse/dependent coverage, disability waiver

Underwriting Type: Often guaranteed or simplified since the insurer spreads risk across a group

Why Choose Group Life Insurance

What makes it better: Group plans offer cost‑effective coverage with minimal paperwork and fast enrollment, unlike individual policies that require medical underwriting.

It solves access barriers to life insurance for employees who might not qualify individually, and enhances overall benefit value.

Who should not buy: Individuals needing lifelong personal coverage may still want an individual policy that follows you regardless of employment.

Supporting Content & Buying Guides

When comparing group life insurance in 2026, employers should evaluate coverage formulas, premium cost sharing, available riders, and administrative ease to best fit workforce needs.

FAQs

1. Do employees need a medical exam?

Often no—group policies commonly use guaranteed or simplified underwriting.

2. How much coverage is typical?

Coverage may be a flat amount or a salary multiple (e.g., 1× pay).

3. Is coverage portable?

Usually not—coverage typically ends when employment ends, though some plans offer conversion options.

4. Can dependents be covered?

Yes—some plans include spouse and child riders.

5. Do employers or employees pay premiums?

Both models exist: employer‑paid, employee‑paid, or shared contributions