Guaranteed Life Insurance

“No exam, no delay, you’re approved right away.”

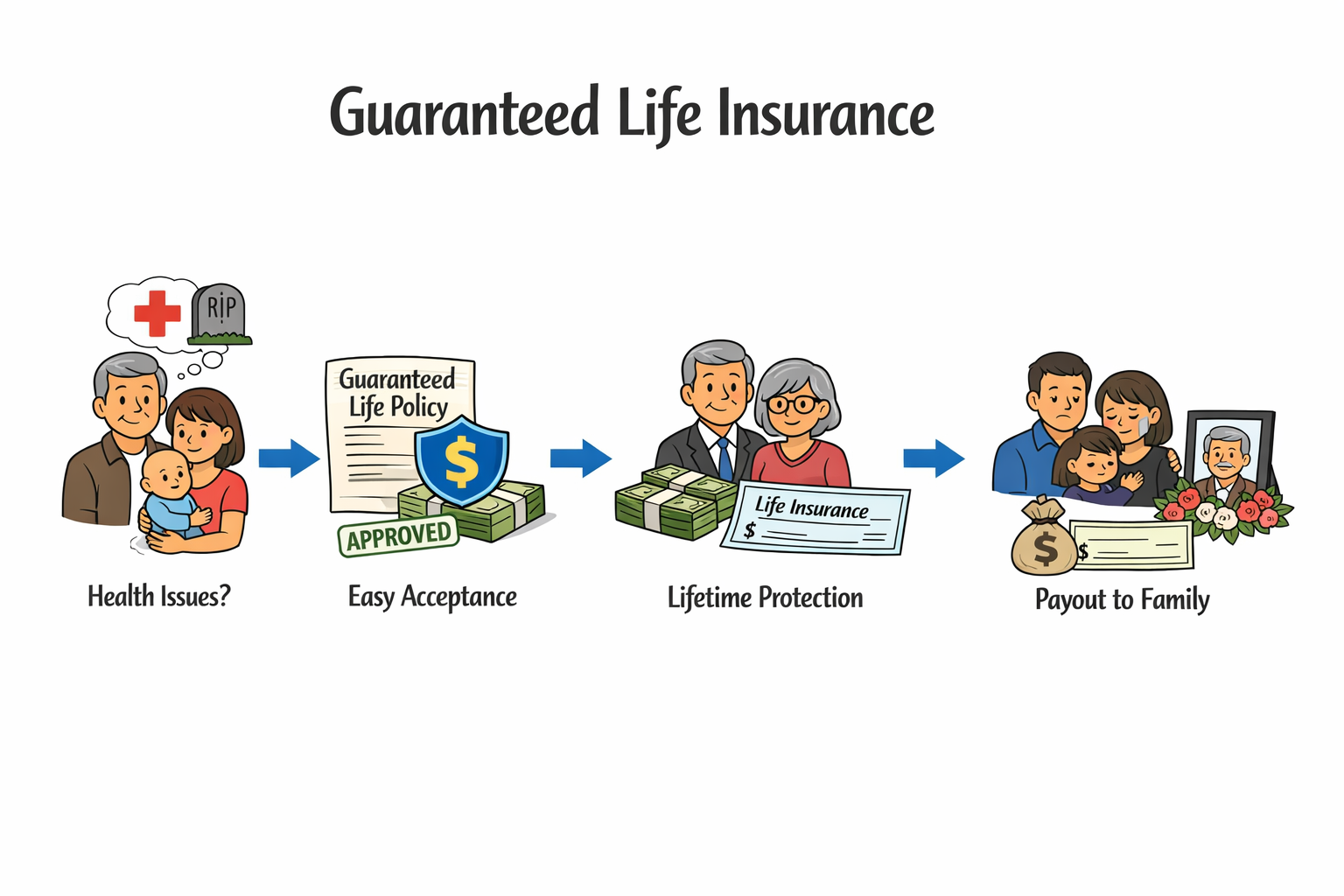

Coverage You Can’t Be Denied

Guaranteed life insurance is a permanent life insurance policy that guarantees acceptance without any medical exam or health questions — so if your health stops you from qualifying for traditional life insurance, you’re still approved as long as you meet the age requirements.

It’s often used by older adults or people with serious health conditions who need financial peace of mind without underwriting barriers. Key benefits include easy qualification, lifelong coverage, and a built‑in cash value component that grows over time.

Real‑world use cases: covering funeral and burial costs, paying off medical bills, creating a small legacy for loved ones, or protecting family from debt after passing.

Policy Details & Specifications

Policy Type: Guaranteed Issue / Guaranteed Acceptance Life Insurance (a form of whole life)

Term Length: Lifetime (no expiration)

Coverage Range: Typically $5,000–$25,000 (varies by carrier)

Eligibility: Usually ages ~45–85, no health questions required

Riders: Some policies may include accelerated or terminal benefit options

Underwriting Type:Guaranteed acceptance (no medical underwriting)

Why Choose Guaranteed Life Insurance

What makes it better: You cannot be turned down for health reasons, which makes this one of the few ways severely ill or elderly applicants can get coverage.

Problems it solves: access to life insurance when traditional underwriting rejects you; funds for final expenses; guaranteed legacy.

Who should not buy: healthy applicants who can qualify for better pricing and higher coverage through traditional or simplified issue policies.

Supporting Content & Buying Guides

Compared with simplified issue or traditional whole life insurance, guaranteed‑issue policies cost more per dollar of coverage and have lower maximum benefits. Always compare quotes and policy terms before choosing.

FAQs

1. Is a medical exam required?

No — guaranteed acceptance means no exams or health questions.

2. When does full coverage start?

Some policies have a waiting period (often 2–3 years) before full benefits are payable for natural causes.

3. How much coverage can I get?

Typically a few thousand to ~$25,000.

4. Are premiums fixed?

Yes — premiums are usually level for life.

5. Who benefits most?

Those who cannot qualify for traditional life insurance due to health or age.